The S&P 500 set a marginal new high on Friday, in the context of a broad rollover in momentum thus far this year that we view as likely – though of course not certain – to represent a broad cyclical peak of the sort that we observed in 2000 and 2007, as distinct from spike-peaks like 1987. Valuation measures remain extreme, with the market capitalization of nonfinancial stocks pushing 130% of GDP (relative to a pre-bubble norm of about 55%), the S&P 500 price/revenue ratio at 1.7, versus a pre-bubble norm of 0.8, and the Shiller P/E near 26 – which while lower than the 2000 extreme, exceeds every pre-bubble observation except for a few months approaching the 1929 peak. We presently estimate 10-year nominal total returns for the S&P 500 Index averaging just 2.3% annually, with zero or negative total returns on every horizon shorter than about 7 years.

A side note about valuations and profit margins – my concern about record profit margins here is emphatically not centered on what profit margins may do over the next few quarters or years. The relationship between cyclical movements in earnings and stock prices is simply not very strong. Rather, as I noted in The Coming Retreat in Corporate Earnings, "my present concern is much more secular in nature. It can be expressed very simply: investors are taking current earnings at face value, as if they are representative of long-term flows, at a time when current earnings are more unrepresentative of those flows than at any time in history. The problem is not simply that earnings are likely to retreat deeply over the next few years. Rather, the problem is that investors have embedded the assumption of permanently elevated profit margins into stock prices, leaving the market about 80-100% above levels that would provide investors with historically adequate long-term returns."

In other words, we should not be concerned about extremely elevated profit margins because earnings are likely to weaken and stock prices might follow over the next couple of years (although that may very well occur). We should be concerned because investors are pricing stocks as a multiple of current earnings. They are implicitly using current earnings as if they are representative and proportional to theentire stream of future earnings going out over the next five decades or more. That's what it means to use a valuation multiple. It means that you take some fundamental as a sufficient statistic for the stream of cash flows that the security will deliver into the hands of investors for decades to come. If you think you know what wage rates, competitive pressures, interest rates and tax policy will be 10, 20, 30, 40 and 50 years from now, and that the present situation is representative and permanent, good luck with that. Otherwise, investors should recognize that because of the variability of profit margins over the long-term, valuation measures that adjust for variations in profit margins have been dramatically more reliable than unadjusted measures over time (see Margins, Multiples, and the Iron Law of Valuation)

Low volatility and suppressed short-term interest rates are a breeding ground for yield-seeking speculation. This reach for yield has now driven junk bond yields to about 5%, which is interesting given that yields are now near or below typical historical default rates. Meanwhile, the majority of new debt issuance today is taking the form of leveraged loans to already highly-indebted borrowers, with "covenant lite" features that provide little recourse in the event of default. This is the sort of behavior that should wake investors up like a triple Espresso. It doesn't because they have been conditioned to focus on yield alone, without considering the minimal amount of capital loss that would wipe that yield out. This is not a new dynamic, and precisely because it is not a new dynamic, one can always find solace from the same Broadway kick-line of dancing clowns that reassured investors that credit was sound, subprime was contained, and stocks were still cheap in 2000 and 2007.

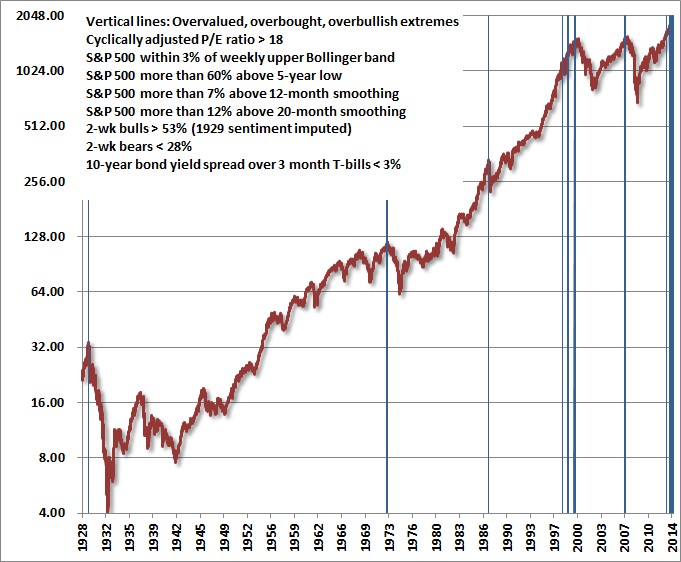

Meanwhile, overbought measures also remain extreme, as investors have become conditioned to a perpetually diagonal advance like those that brought stocks to similarly overvalued, overbought, overbullish pinnacles throughout history (see The Journeys of Sisyphus). As I've often noted, there are countless ways to operationalize the concept of "overvalued, overbought, overbullish" depending on the severity of the condition one wishes to capture. Conditions that capture less severe market peaks also tend to include various false signals, while more restrictive conditions limit the set to the worst pre-crash peaks in history, but will tend to miss cyclical peaks that were less extreme). The following set of criteria falls into the more restrictive category, and limits the set to the 1929, 1972, 1987 peaks, three tech-bubble instances (the peak before the 1998 Asian crisis, a pre-correction peak in 1999, and the 2000 top), the 2007 peak, and of course, a solid band of warnings today. From our perspective, this time is different only in the extended period over which these and similar conditions have been sustained in recent quarters without consequence.

Continue reading here.

Also check out: John Hussman Undervalued Stocks John Hussman Top Growth Companies John Hussman High Yield stocks, and Stocks that John Hussman keeps buyingAbout the author:Canadian Valuehttp://valueinvestorcanada.blogspot.com/

| Currently 0.00/512345 Rating: 0.0/5 (0 votes) | |

Subscribe via Email

Subscribe RSS Comments Please leave your comment:

More GuruFocus Links

| Latest Guru Picks | Value Strategies |

| Warren Buffett Portfolio | Ben Graham Net-Net |

| Real Time Picks | Buffett-Munger Screener |

| Aggregated Portfolio | Undervalued Predictable |

| ETFs, Options | Low P/S Companies |

| Insider Trends | 10-Year Financials |

| 52-Week Lows | Interactive Charts |

| Model Portfolios | DCF Calculator |

RSS Feed  | Monthly Newsletters |

| The All-In-One Screener | Portfolio Tracking Tool |

MORE GURUFOCUS LINKS

| Latest Guru Picks | Value Strategies |

| Warren Buffett Portfolio | Ben Graham Net-Net |

| Real Time Picks | Buffett-Munger Screener |

| Aggregated Portfolio | Undervalued Predictable |

| ETFs, Options | Low P/S Companies |

| Insider Trends | 10-Year Financials |

| 52-Week Lows | Interactive Charts |

| Model Portfolios | DCF Calculator |

| RSS Feed | Monthly Newsletters |

| The All-In-One Screener | Portfolio Tracking Tool |

SPY STOCK PRICE CHART

191.44 (1y: +16%) $(function(){var seriesOptions=[],yAxisOptions=[],name='SPY',display='';Highcharts.setOptions({global:{useUTC:true}});var d=new Date();$current_day=d.getDay();if($current_day==5||$current_day==0||$current_day==6){day=4;}else{day=7;} seriesOptions[0]={id:name,animation:false,color:'#4572A7',lineWidth:1,name:name.toUpperCase()+' stock price',threshold:null,data:[[1369803600000,165.22],[1369890000000,165.83],[1369976400000,163.45],[1370235600000,164.35],[1370322000000,163.56],[1370408400000,161.27],[1370494800000,162.73],[1370581200000,164.8],[1370840400000,164.8],[1370926800000,163.1],[1371013200000,161.75],[1371099600000,164.21],[1371186000000,163.18],[1371358800000,163.18],[1371445200000,164.44],[1371531600000,165.74],[1371618000000,163.45],[1371704400000,159.4],[1371790800000,159.07],[1372050000000,157.06],[1372136400000,158.58],[1372222800000,160.14],[1372309200000,161.08],[1372395600000,160.42],[1372654800000,161.36],[1372741200000,161.21],[1372827600000,161.28],[1372914000000,161.28],[1373000400000,163.02],[1373259600000,163.95],[1373346000000,165.13],[1373432400000,165.19],[1373518800000,167.44],[1373605200000,167.51],[1373864400000,168.16],[1373950800000,167.53],[1374037200000,167.95],[1374123600000,168.87],[1374210000000,169.17],[1374469200000,169.5],[1374555600000,169.14],[1374642000000,168.52],[1374728400000,168.93],[1374814800000,169.11],[1375074000000,168.59],[1375160400000,168.59],[1375246800000,168.71],[1375333200000,170.66],[1375419600000,170.95],[1375678800000,170.7],[1375765200000,169.73],[1375851600000,169.18],[1375938000000,169.8],[1376024400000,169.31],[1376283600000,169.11],[1376370000000,169.61],[1376456400000,168.74],[1376542800000,166.38],[1376629200000,165.83],[1376888400000,164.77],[1376974800000,165.58],[1377061200000,164.56],[1377147600000,166.06],[1377234000000,166.62],[1377493200000,166],[1377579600000,163.33],[1377666000000,163.91],[1377752400000,164.17],[1377838800000,163.65],[1378098000000,163.65],[1378184400000,164.39],[1378270800000,165.75],[1378357200000,165.96],[1378443600000,166.04],[1378702800000,167.63],[1378789200000,168.87],[1378875600000,169.4],[1378962000000,168.95],[1379048400000,169.33],[1379307600000,170.31],[1379394000000,171.07],[1379480400000,173.05],[1379566800000,172.76],[1379653200! 000,170.72],[1379912400000,169.93],[1379998800000,169.53],[1380085200000,169.04],[1380171600000,169.69],[1380258000000,168.91],[1380517200000,168.01],[1380603600000,169.34],[1380690000000,169.18],[1380776400000,167.62],[1380862800000,168.89],[1381122000000,167.43],[1381208400000,165.48],[1381294800000,165.6],[1381381200000,169.17],[1381467600000,170.26],[1381726800000,170.94],[1381813200000,169.7],[1381899600000,172.07],[1381986000000,173.22],[1382072400000,174.39],[1382331600000,174.4],[1382418000000,175.41],[1382504400000,174.57],[1382590800000,175.15],[1382677200000,175.95],[1382936400000,176.23],[1383022800000,177.17],[1383109200000,176.29],[1383195600000,175.79],[1383282000000,176.21],[1383544800000,176.83],[1383631200000,176.27],[1383717600000,177.17],[1383804000000,174.93],[1383890400000,177.29],[1384149600000,177.32],[1384236000000,176.96],[1384322400000,178.38],[1384408800000,179.27],[1384495200000,180.05],[1384754400000,179.42],[1384840800000,179.03],[1384927200000,178.47],[1385013600000,179.91],[1385100000000,180.81],[1385359200000,180.63],[1385445600000,180.68],[1385532000000,181.12],[1385618400000,181.12],[1385704800000,181],[1385964000000,180.53],[1386050400000,179.75],[1386136800000,179.73],[1386223200000,178.94],[1386309600000,180.94],[1386568800000,181.4],[1386655200000,180.75],[1386741600000,178.72],[1386828000000,178.13],[1386914400000,178.11],[1387173600000,179.22],[1387260000000,178.65],[1387346400000,181.7],[1387432800000,181.49],[1387519200000,181.56],[1387778400000,182.53],[1387864800000,182.93],[1387951200000,182.93],[1388037600000,183.86],[1388124000000,183.85],[1388383200000,183.82],[1388469600000,184.69],[1388556000000,184.69],[1388642400000,182.92],[1388728800000,182.89],[1388988000000,182.36],[1389074400000,183.48],[1389160800000,183.52],[1389247200000,183.64],[1389333600000,184.14],[1389592800000,181.69],[1389679200000,183.67],[1389765600000,184.66],[1389852000000,184.42],[1389938400000,183.64],[1390197600000,183.64],[1390284000000,184.18],[1390370400000,184.3],[1390456800! 000,182.7! 9],[1390543200000,178.89],[1390802400000,178.01],[1390888800000,179.07],[1390975200000,177.35],[1391061600000,179.23],[1391148000000,178.18],[1391407200000,174.17],[1391493600000,175.39],[1391580000000,175.17],[1391666400000,177.48],[1391752800000,179.68],[1392012000000,180.01],[1392098400000,181.98],[1392184800000,182.07],[1392271200000,183.01],[1392357600000,184.02],[1392616800000,184.02],[1392703200000,184.24],[1392789600000,183.02],[1392876000000,184.1],[1392962400000,183.89],[1393221600000,184.91],[1393308000000,184.84],[1393394400000,184.85],[1393480800000,185.82],[1393567200000,

Nick Ut/AP NEW YORK -- A monthly gauge of U.S. consumer sentiment fell in May as a gloomy view on income growth clouded an otherwise positive economic outlook, a survey released Friday showed. The Thomson Reuters/University of Michigan's final May reading on the overall index on consumer sentiment came in at 81.9, down from 84.1 the month before. It was also below the expectation of 82.5 among economists polled by Reuters. However it did show a slight increase from the preliminary reading issued on May 16. "The slippage in consumer confidence came to a halt in late May," survey director Richard Curtin said in a statement. Curtin said the level may have declined by 2.2 points since April, but when averaging in the first four months of the year, the May figure was slightly above the average of 81.7. "At present, the economy was anticipated to be strong enough in the year ahead to produce the best change in job prospects since 2004," Curtin said, "The main concern expressed by consumers involved dismal prospects for wage growth, which for nearly half of all households meant anticipated declines in inflation-adjusted incomes and living standards during the year ahead," he added. Some 56 percent of consumers reported that the economy had improved, up from 49 percent in April. The survey's barometer of current economic conditions fell to 94.5 from 98.7 in April and below a forecast of 95.8. The gauge of consumer expectations slipped to 73.7 from 74.7 and fell short of an expected 74.0. The survey's one-year inflation expectation rose to 3.3 percent from last month at 3.2 percent, while the survey's five-to-10-year inflation outlook fell to 2.8 percent from 2.9 percent in April.

Nick Ut/AP NEW YORK -- A monthly gauge of U.S. consumer sentiment fell in May as a gloomy view on income growth clouded an otherwise positive economic outlook, a survey released Friday showed. The Thomson Reuters/University of Michigan's final May reading on the overall index on consumer sentiment came in at 81.9, down from 84.1 the month before. It was also below the expectation of 82.5 among economists polled by Reuters. However it did show a slight increase from the preliminary reading issued on May 16. "The slippage in consumer confidence came to a halt in late May," survey director Richard Curtin said in a statement. Curtin said the level may have declined by 2.2 points since April, but when averaging in the first four months of the year, the May figure was slightly above the average of 81.7. "At present, the economy was anticipated to be strong enough in the year ahead to produce the best change in job prospects since 2004," Curtin said, "The main concern expressed by consumers involved dismal prospects for wage growth, which for nearly half of all households meant anticipated declines in inflation-adjusted incomes and living standards during the year ahead," he added. Some 56 percent of consumers reported that the economy had improved, up from 49 percent in April. The survey's barometer of current economic conditions fell to 94.5 from 98.7 in April and below a forecast of 95.8. The gauge of consumer expectations slipped to 73.7 from 74.7 and fell short of an expected 74.0. The survey's one-year inflation expectation rose to 3.3 percent from last month at 3.2 percent, while the survey's five-to-10-year inflation outlook fell to 2.8 percent from 2.9 percent in April. Getty Images

Getty Images

Agence France-Presse/Getty Images

Agence France-Presse/Getty Images

Bond yields hitting 3%? Not so fast!

Bond yields hitting 3%? Not so fast!  Popular Posts: 5 Crash-Proof Dividend Stocks9 Cheap Stocks to Buy Now for $10 or LessTesla Stock Could Fall Even Lower on Battery Boondoggle Recent Posts: 11 Retailers to Dump Now Why You Don’t Have Enough Saved for Retirement JCPenney Rally Just a Head Fake – Don’t Buy JCP Stock View All Posts

Popular Posts: 5 Crash-Proof Dividend Stocks9 Cheap Stocks to Buy Now for $10 or LessTesla Stock Could Fall Even Lower on Battery Boondoggle Recent Posts: 11 Retailers to Dump Now Why You Don’t Have Enough Saved for Retirement JCPenney Rally Just a Head Fake – Don’t Buy JCP Stock View All Posts  First, we started the year with a spate of bad weather that depressed both hiring and spending trends. Then, after what seemed like a snap-back in March, we were greeted by a meager 0.1% rise in April retail sales according to the latest data.

First, we started the year with a spate of bad weather that depressed both hiring and spending trends. Then, after what seemed like a snap-back in March, we were greeted by a meager 0.1% rise in April retail sales according to the latest data. Returns since 1/1/14: -28% vs. 3% gains for the S&P 500.

Returns since 1/1/14: -28% vs. 3% gains for the S&P 500. Returns since 1/1/14: -24%

Returns since 1/1/14: -24%

Returns since 1/1/14: -24%

Returns since 1/1/14: -24% Returns since 1/1/14: +13%

Returns since 1/1/14: +13% Returns since 1/1/14: -15%

Returns since 1/1/14: -15% Returns since 1/1/14: -2%

Returns since 1/1/14: -2% Returns since 1/1/14: -24%

Returns since 1/1/14: -24% Returns since 1/1/14: -23%

Returns since 1/1/14: -23% Returns since 1/1/14: -12%

Returns since 1/1/14: -12% Returns since 1/1/14: -32%

Returns since 1/1/14: -32% Peter Dazeley, Getty Images Earlier this month, PerkStreet, an online bank that provided cash-back rewards for using your debit card, announced that it would be shutting down. That was disappointing news for account holders, but nobody lost their life savings: Their funds were all FDIC-insured, so they can still retrieve their money. However, the same could not be said of their rewards. PerkStreet executives remorsefully explained that they "just didn't have the financial capability to pay out perks earned," so anyone with an unclaimed rewards balance as of the announcement lost their accrued cash-back. Many account holders had spent months or years earning rewards with their debit cards, so some customers lost a significant amount of money. "I just lost $500 in perks with no warning," wrote one angry user. "I've been saving those for a long time, for special occasions and to treat myself." "We were sitting on almost $300 in perks saving it for an anniversary cruise," complained another user. Yet another said he'd lost $500 that he'd planned to use to buy Christmas presents. Unfortunately, there's nothing these customers can do about it, because they don't actually own their rewards points. That may come as a surprise to most people, because federal law provides ample protection for consumers in their banking transactions: Whether your bank goes bust or your credit card gets stolen, your money is safe. But even though rewards are presented in commercials as the primary reason to open a new credit card, they're treated in the fine print as an add-on that can be changed or taken away at any time. "The credit card companies' viewpoint about rewards programs is that they are just an extra benefit that they offer at their discretion, and they're doing you a favor," says Odysseas Papadamitriou of credit card tracking site CardHub.com. "But for a significant portion of the customer base, the main reason they use the card is the rewards. It's like a hotel saying that having a shower is just a luxury they give you, and if the shower doesn't work, you should shut your mouth about it." And, frustrating as it may be, there are several ways that your hard-earned rewards points can disappear on you. You don't pay your bill. This is the one that makes the most sense. It may seem like you're earning rewards every time you use your card, but keep in mind that you haven't actually spent any money until you've paid off your bill for that time period. "If you miss the payment period, they'll hold the rewards," says Alex Matjanec, co-founder of MyBankTracker. As he explains, though, your rewards aren't permanently wiped out -- American Express, for instance, will give you the rewards you earned if you pay off your whole debt and a $35 fee. You somehow violate the terms of your cardholder agreement. There are numerous ways that you can game the system to get more credit card rewards. But if your issuing bank figures out that you're doing something fishy, it could cancel your account, blocking access to your rewards in the process. That's what happened to this man, who had more than $2,400 in rewards points revoked by Chase after it apparently raised an eyebrow at what he had to spend to earn them. Only after intervention by local media did the bank give him the rewards he'd earned. "The terms and conditions say they can close the account at their own discretion for any reason," says NerdWallet's Anisha Sekar, who points to illegal activity like online gambling as one reason a bank might shut you down. "You pretty much serve at the mercy of the bank." The rewards program decides to devalue its points. In April, CardHub's Papadamitriou got a letter from American Express with some bad news: The travel rewards points he'd accrued with his Hilton HHonors Card were being devalued. The good news was that he had about a month and a half too book travel at the current rate before the new system kicked in. But once June 15 rolled around, he would need more points to get a free hotel stay. That wasn't an isolated incident, by the way: Earlier this year, the three major hotel chains -- Marriott, Hilton and Starwood -- all made it more expensive to use credit card rewards points to book hotel stays. Cardholders still got the same amount of points for their purchases, but they were no longer worth as much as they used to be. The bank shuts down. This is what happened to PerkStreet, though it must be said that this is a rare occurrence. PerkStreet was a startup, and was thus heavily reliant on securing funding to keep its doors open. A major bank like Chase, Citi or Bank of America is incredibly unlikely to suddenly shutter its operations. Still, big banks aren't the only platforms that allow you to earn rewards -- there are, for instance, a number of deal sites that provide rewards when you buy a product after following a link from their site. While there's no reason to believe that any of these sites are in danger of going under, just bear in mind that not everyone who provides rewards is as secure as the titans of the banking industry. Your account is inactive. If it's been several months since you've earned any Hilton HHonors points, expect to get an email that goes something like this: "We haven't noticed any activity on your HHonors account in more than nine months. Remember, to keep your account active, you must earn HHonors points at least once every 12 months. Otherwise, all of your points may be forfeited." Hilton is hardly alone in requiring regular account activity for customers to keep the rewards they've earned. Credit.com points to the BarclayCard's NFL ExtraPoints Card, which will close your account if you go six months without charging anything to it. And it also notes that points and miles can expire if not used within a certain time frame. So how can you avoid forfeiting your hard-earned points? As always, start by reading the fine print, where you'll find all sorts of information on expiration dates and unauthorized account activity. But your best bet is to just redeem your points on a regular basis so you never build up a large balance that can be taken away. "People are treating their rewards points as a savings account, and they shouldn't be thinking about it that way," says Matjanec. "I think it's just the excitement of seeing that number grow." But if something goes wrong, you also have to deal with the despair of seeing that number disappear. So, if you have a significant stash of unused reward points, use them to buy something -- or cash them in and stash the bonus dough in the secure confines of a a savings account.

Peter Dazeley, Getty Images Earlier this month, PerkStreet, an online bank that provided cash-back rewards for using your debit card, announced that it would be shutting down. That was disappointing news for account holders, but nobody lost their life savings: Their funds were all FDIC-insured, so they can still retrieve their money. However, the same could not be said of their rewards. PerkStreet executives remorsefully explained that they "just didn't have the financial capability to pay out perks earned," so anyone with an unclaimed rewards balance as of the announcement lost their accrued cash-back. Many account holders had spent months or years earning rewards with their debit cards, so some customers lost a significant amount of money. "I just lost $500 in perks with no warning," wrote one angry user. "I've been saving those for a long time, for special occasions and to treat myself." "We were sitting on almost $300 in perks saving it for an anniversary cruise," complained another user. Yet another said he'd lost $500 that he'd planned to use to buy Christmas presents. Unfortunately, there's nothing these customers can do about it, because they don't actually own their rewards points. That may come as a surprise to most people, because federal law provides ample protection for consumers in their banking transactions: Whether your bank goes bust or your credit card gets stolen, your money is safe. But even though rewards are presented in commercials as the primary reason to open a new credit card, they're treated in the fine print as an add-on that can be changed or taken away at any time. "The credit card companies' viewpoint about rewards programs is that they are just an extra benefit that they offer at their discretion, and they're doing you a favor," says Odysseas Papadamitriou of credit card tracking site CardHub.com. "But for a significant portion of the customer base, the main reason they use the card is the rewards. It's like a hotel saying that having a shower is just a luxury they give you, and if the shower doesn't work, you should shut your mouth about it." And, frustrating as it may be, there are several ways that your hard-earned rewards points can disappear on you. You don't pay your bill. This is the one that makes the most sense. It may seem like you're earning rewards every time you use your card, but keep in mind that you haven't actually spent any money until you've paid off your bill for that time period. "If you miss the payment period, they'll hold the rewards," says Alex Matjanec, co-founder of MyBankTracker. As he explains, though, your rewards aren't permanently wiped out -- American Express, for instance, will give you the rewards you earned if you pay off your whole debt and a $35 fee. You somehow violate the terms of your cardholder agreement. There are numerous ways that you can game the system to get more credit card rewards. But if your issuing bank figures out that you're doing something fishy, it could cancel your account, blocking access to your rewards in the process. That's what happened to this man, who had more than $2,400 in rewards points revoked by Chase after it apparently raised an eyebrow at what he had to spend to earn them. Only after intervention by local media did the bank give him the rewards he'd earned. "The terms and conditions say they can close the account at their own discretion for any reason," says NerdWallet's Anisha Sekar, who points to illegal activity like online gambling as one reason a bank might shut you down. "You pretty much serve at the mercy of the bank." The rewards program decides to devalue its points. In April, CardHub's Papadamitriou got a letter from American Express with some bad news: The travel rewards points he'd accrued with his Hilton HHonors Card were being devalued. The good news was that he had about a month and a half too book travel at the current rate before the new system kicked in. But once June 15 rolled around, he would need more points to get a free hotel stay. That wasn't an isolated incident, by the way: Earlier this year, the three major hotel chains -- Marriott, Hilton and Starwood -- all made it more expensive to use credit card rewards points to book hotel stays. Cardholders still got the same amount of points for their purchases, but they were no longer worth as much as they used to be. The bank shuts down. This is what happened to PerkStreet, though it must be said that this is a rare occurrence. PerkStreet was a startup, and was thus heavily reliant on securing funding to keep its doors open. A major bank like Chase, Citi or Bank of America is incredibly unlikely to suddenly shutter its operations. Still, big banks aren't the only platforms that allow you to earn rewards -- there are, for instance, a number of deal sites that provide rewards when you buy a product after following a link from their site. While there's no reason to believe that any of these sites are in danger of going under, just bear in mind that not everyone who provides rewards is as secure as the titans of the banking industry. Your account is inactive. If it's been several months since you've earned any Hilton HHonors points, expect to get an email that goes something like this: "We haven't noticed any activity on your HHonors account in more than nine months. Remember, to keep your account active, you must earn HHonors points at least once every 12 months. Otherwise, all of your points may be forfeited." Hilton is hardly alone in requiring regular account activity for customers to keep the rewards they've earned. Credit.com points to the BarclayCard's NFL ExtraPoints Card, which will close your account if you go six months without charging anything to it. And it also notes that points and miles can expire if not used within a certain time frame. So how can you avoid forfeiting your hard-earned points? As always, start by reading the fine print, where you'll find all sorts of information on expiration dates and unauthorized account activity. But your best bet is to just redeem your points on a regular basis so you never build up a large balance that can be taken away. "People are treating their rewards points as a savings account, and they shouldn't be thinking about it that way," says Matjanec. "I think it's just the excitement of seeing that number grow." But if something goes wrong, you also have to deal with the despair of seeing that number disappear. So, if you have a significant stash of unused reward points, use them to buy something -- or cash them in and stash the bonus dough in the secure confines of a a savings account.